Learn » Blog » Inflation woes: encouraging headlines vs. feeling poorer

Inflation woes: encouraging headlines vs. feeling poorer

Published on 05/11/2024

Topics:

Research Hub

By Shamubeel Eaqub, Chief Economist, Simplicity Research Hub

Inflation might be cooling down, but it’s still leaving a chill on household budgets.

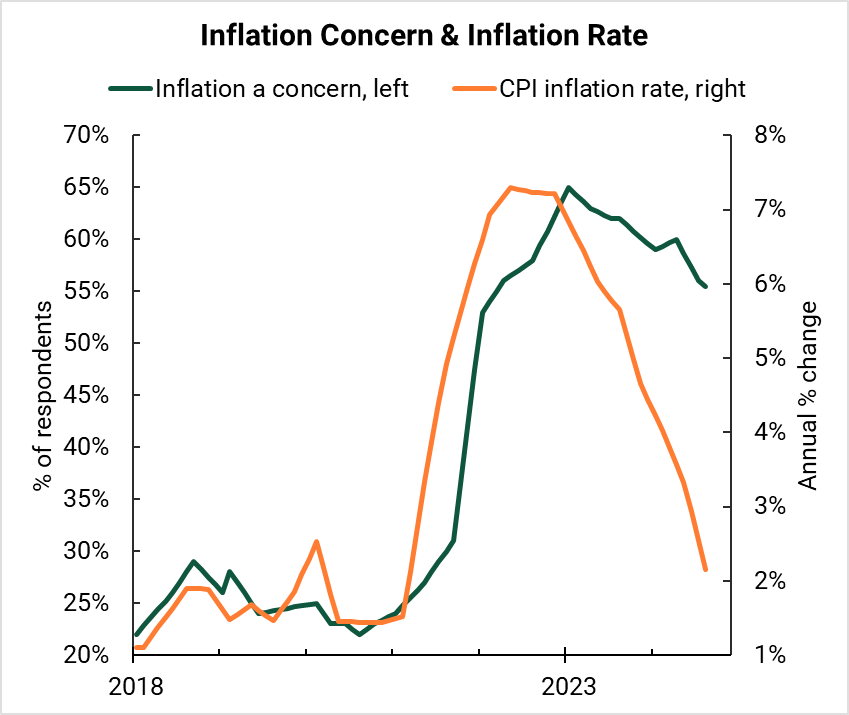

New Zealand's reported inflation rate has slowed from a peak of over 7% to a more “normal” 2%. Yet inflation remains a top concern among Kiwis. According to a recent IPSOS survey [1], it’s the number one worry on people’s minds. Why? Because a lower inflation rate doesn’t mean prices are falling; it just means they’re rising more slowly. At the household level, it still feels like money isn’t going very far and job prospects are uncertain.

Figure 1: Inflation concern vs actual inflation rate

Apparent paradox

Why this paradox? This feeling isn’t unique to New Zealand. In the US, there is a big gap between what is a currently strong economy and the fairly negative perceptions of many Americans. A report by the Brookings Institution unpacked some of the things driving this - the lasting impact of inflation (both the rate of change and level of prices), media/social media amplification of negative news and political biases influencing views on the economy [2].

This could inform the apparent divergence in New Zealand between a moderation in inflation rate and households reporting inflation as a top worry. The data suggests that it is mainly to do with two key things:

-

Inflation concerns take time to flow through to consumer concerns (the pain of higher prices creeps up over time; relief also comes slowly as people’s perceptions change)

-

Inflation has eroded spending power. That is, people feel poorer and their finances are still under pressure.

The IPSOS survey did not suggest a strong political bias in New Zealand. Statistically there appears to be some 'upward bias' from high inflation. This means that perceptions appear to be more affected by accelerating inflation than slowing inflation.

Not just perception

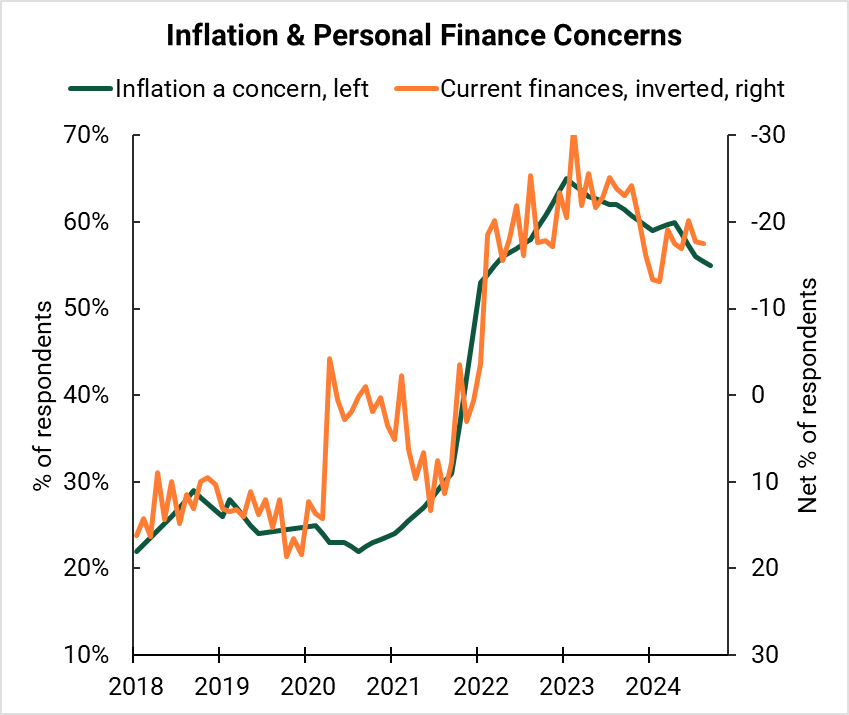

While perception does play a role, the financial stress many feel is rooted in reality.

The ANZ-Roy Morgan Consumer Confidence survey asks people if they feel financially better off compared to a year ago. The chart below shows that inflation as a concern closely correlates with peoples’ perceptions of current finances, which is mainly to do with people's income prospects and spending ability.

Figure 2: Relationship between inflation & personal finance concerns

There was a divergence when the pandemic began. Wages grew slowly but were quickly outpaced by rising prices. This reduced people’s real income, which can be seen in the chart below. It was also a period of heightened uncertainty, especially around job prospects.

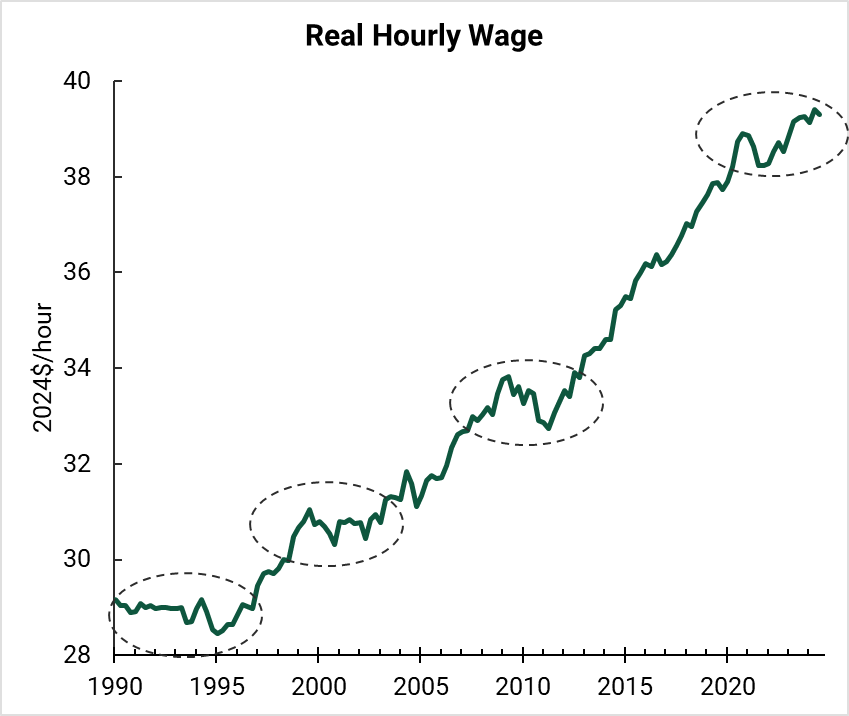

The chart below also shows that real wages (wages after the cost of living has been factored) fall or stagnate during every recession.

Consumer fears appear to be based on both the erosion of purchasing power in recent years due to high inflation, and on reduced income prospects in the coming months. The latter being because the labour market is weak (there are job losses, wages are growing very slowly and job ads have slumped, meaning there are fewer job and career opportunities).

Figure 3: Real hourly wage (after cost of living)

It will get better and help is available

Perceptions matter - because confidence is a necessary but not sufficient condition for people to make decisions around spending, investing and jobs (or other big decisions). Right now consumers are still living in the aftermath of high inflation and reduced spending power. While inflation is moderating, a weaker labour market may keep finances under pressure for a bit longer.

There are signs that the recession is nearing the bottom. Leading indicators are stabilising or lifting. But the economy doesn't turn on a dime. More job losses and business closures are likely in the coming months.

However there is relief on the horizon. Falling mortgage rates will be welcomed by about a third of households. But for lower income renters, the relief may be slower to come. And for retirees, falling interest rates may risk reducing their income from savings. For many other families it will not feel much like a recovery until perhaps the middle of next year (2025). Until then, ask for help if you need it. MoneyTalks is a good starting point, or reach out to family and friends.

www.moneytalks.co.nz | 0800 345 123