Learn » Simplicity Research Hub » KiwiSaver 2.0: Why increasing contributions is only the first step

KiwiSaver 2.0: Why increasing contributions is only the first step

Published on 24/11/2025

By Shamubeel Eaqub, Chief Economist - Simplicity Research Hub

Increasing KiwiSaver contributions to 12.5%, as Christopher Luxon announced as an election policy, is a great step in the right direction. It follows NZ First’s support for a compulsory scheme, and together these signals suggest something important - change is coming.

The 2026 General Election is shaping up to be the first step toward KiwiSaver 2.0. Since its inception, changes to the scheme have largely weakened it. But there is now broader acceptance that a strengthened KiwiSaver will be essential for a well-functioning retirement system in the future.

The current model isn’t sustainable

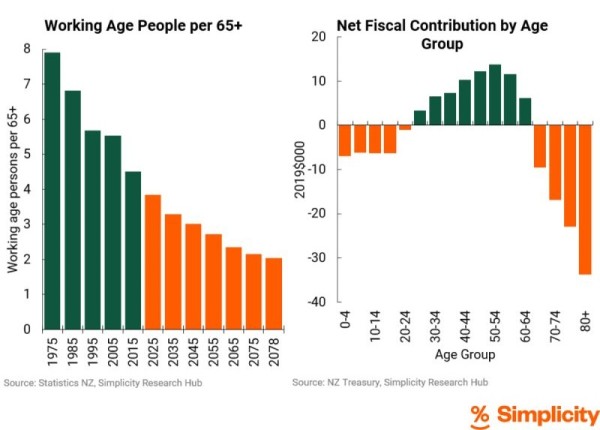

Our mix of public services and taxes only works with around five working-age people per retiree. We’re already below that at four, and this ratio will continue to fall - steadily tracking toward two workers per retiree within 50 years. KiwiSaver is just one part of the solution, but an increasingly important one.

Simply increasing contribution rates, however, won’t be enough. On its own, it risks further encouraging low or precarious-income New Zealanders to opt out of contributing altogether.

Figure 1: Working age people per retiree. NZ's current fiscal promises (public services & tax settings) need around 5 working age people per retiree. But we are aging fast, and we don't have enough working age people already. It will become harder unless we make gradual changes from now.

There are practical ways to fix this

1. Decouple employee and employer contributions

Make employer contributions mandatory for all forms of work, including self-employment. This would formalise KiwiSaver as a quasi-mandatory tier 2* pension scheme designed to ensure an adequate retirement income.

Employer rates would act as a minimum contribution threshold. Employees could still make voluntary top-ups, but wouldn’t need to in order to receive the employer’s contribution.

This approach aligns with common international practice and creates a fairer structure. Employers can still choose to contribute above the minimum rate - as many already do - but low-wage employers would no longer be perversely incentivised to encourage opt-outs. Crucially, employees would receive the full benefit of employer contributions regardless of their financial situation.

2. Gradually increase contribution rates

Lift rates by 0.5% per year over 13 years to reach 12.5% in the late 2030s. Signposting this well in advance is important, giving firms and workers time to adjust and letting the economic impact pass through slowly into wages. Fears of a major new business costs are misplaced - these contributions would be gradually built into normal employee compensation.

3. Improve access during financial hardship

Increase access to KiwiSaver assets in times of genuine financial distress, potentially through the use of sidecar accounts. It doesn’t make sense to punish low-income households by locking up every dollar for future retirement income when they are in immediate difficulty.

4. Retarget the government contribution to children

Re-design the government subsidy as a universal KiwiSaver contribution for kids, as Max Rashbrooke recently proposed (Kids KiwiSaver: Building national savings, one child at a time). Personally, I would like to see $10 a week for every child from birth, with access for education or training from age 18.

A positive shift in the political landscape

With MMP, we don’t need every political party to offer the perfect policy. What matters is that we’re seeing an encouraging shift - politicians of different stripes are now looking seriously at how KiwiSaver can help address our ageing population.

This is very welcome.